When it comes to purchasing a car, one of the biggest decisions you’ll face is whether to finance a new or used vehicle. Each option comes with its own set of advantages and disadvantages, and understanding these factors can help you make an informed decision based on your budget, lifestyle, and long-term goals. This article explores the pros and cons of financing both a new and a used car, giving you the necessary insights to choose the best option for your needs.

Pros of Financing a New Car

1. Warranty and Reliability

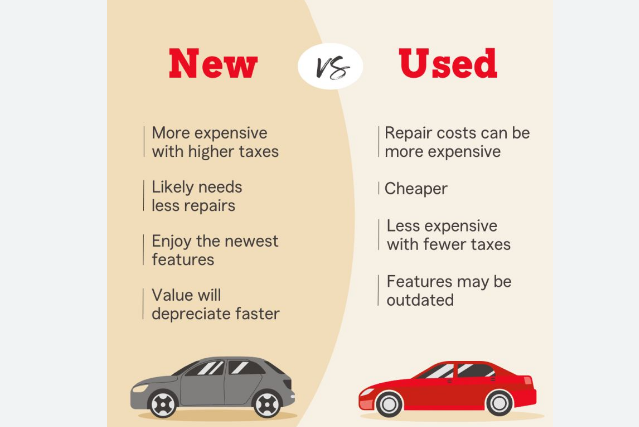

One of the biggest advantages of buying a new car is the warranty. New cars come with a manufacturer’s warranty that typically covers several years or a certain number of miles. This warranty can significantly reduce your out-of-pocket expenses for repairs and maintenance, providing you with peace of mind.

Additionally, new cars are generally more reliable than used cars. They have fewer miles on the odometer, and their mechanical and electrical components are less likely to break down. This means fewer visits to the mechanic, which can save you both time and money.

2. Latest Technology and Features

New cars often come equipped with the latest technology and safety features. If you value features like advanced driver assistance systems (ADAS), infotainment systems, smartphone connectivity, or the latest fuel-efficiency technologies, a new car is likely your best option. These advancements can enhance your driving experience, improve safety, and even help reduce long-term operating costs (such as better fuel economy).

3. Financing Incentives

When financing a new car, dealerships often offer attractive incentives, such as low-interest rates, cash rebates, and special financing offers. If you have good credit, you may be eligible for 0% APR financing or other favorable loan terms, making it easier and more affordable to finance a new car.

4. Customization

With a new car, you have the option to choose the exact specifications you want. From the color and trim level to the features and add-ons, buying new gives you the ability to build your car to your personal preferences. This level of customization isn’t typically available with used cars.

Cons of Financing a New Car

1. Higher Purchase Price

New cars are significantly more expensive than used cars, and this higher cost can lead to larger monthly payments if you finance the vehicle. While you may qualify for low-interest rates, the higher purchase price means you’ll end up paying more overall for the car. This can stretch your budget and lead to long-term financial strain.

2. Depreciation

One of the biggest drawbacks of purchasing a new car is depreciation. As soon as you drive a new car off the lot, it begins to lose value. On average, new cars lose about 20% of their value within the first year and continue to depreciate rapidly over the next few years. This means that if you decide to sell or trade in your car within a few years, you might not recoup a significant portion of what you paid for it.

3. Higher Insurance Costs

New cars tend to be more expensive to insure than used cars. This is because the replacement cost of a new car is higher, and insurance premiums reflect the potential cost of replacing the car in case of an accident. Comprehensive and collision coverage, which is often required when financing a new car, can add to your overall insurance costs.

Pros of Financing a Used Car

1. Lower Purchase Price

One of the most significant advantages of financing a used car is the lower purchase price. Used cars have already gone through the initial depreciation, which means they tend to be much cheaper than their new counterparts. Lower purchase prices lead to lower monthly payments, making it more affordable to finance a used car. If you have a limited budget, buying used can help you get a higher-end model or a more feature-rich car for the same price as a new, base-model vehicle.

2. Slower Depreciation

Depreciation is a major issue when financing a new car, but used cars typically have already gone through the steepest part of their depreciation curve. While used cars still lose value over time, they do so at a slower rate compared to new cars. This means that the value of your car won’t drop as rapidly, and you may be able to sell it for a higher price later on, minimizing your loss.

3. Lower Insurance Costs

Used cars are generally cheaper to insure than new cars because their replacement value is lower. As a result, you may be able to save money on your car insurance premiums. This is particularly beneficial if you’re looking to reduce your overall vehicle-related expenses. With a used car, you may not need to carry as extensive of an insurance policy, allowing for even more savings.

4. Potential for Better Financing Terms

While new car loans may come with attractive incentives, it’s worth noting that used car financing can sometimes offer better overall terms when compared to financing a new car of the same price. Used cars typically require a smaller loan amount, which can help reduce your monthly payments. Additionally, some lenders may offer competitive interest rates on used cars, especially if the car is only a few years old and still in good condition.

Cons of Financing a Used Car

1. Higher Maintenance and Repair Costs

While used cars are often more affordable upfront, they may come with higher maintenance and repair costs. A used vehicle might be older, with more miles on the odometer, meaning it could require more frequent repairs or replacements of key parts, such as tires, brakes, or the transmission. These costs can add up, making it more expensive to own and operate a used car in the long run.

Used cars may also come without a warranty, or with a limited warranty that doesn’t cover all potential repairs. Without the peace of mind provided by a new car’s warranty, you could find yourself paying for unexpected repairs out-of-pocket.

2. Limited Selection and Customization

When buying a used car, you may not find the exact make, model, color, and features you want. Since used cars are pre-owned, the selection is limited, and you may have to compromise on certain features or find a car that meets your needs without being able to customize it. If having the latest technology or specific features is important to you, a used car may not be the best option.

3. Shorter Loan Terms and Higher Interest Rates

Because used cars are cheaper than new ones, lenders may offer shorter loan terms for used car purchases, which could lead to higher monthly payments. Additionally, interest rates on used car loans are often higher than those on new car loans. This means that, even though you’re financing a less expensive vehicle, the higher interest rate can offset some of the savings you might have gained from buying used.

4. Risk of Hidden Problems

With a used car, there’s always the risk of hidden mechanical or electrical issues that may not be immediately apparent during the test drive or pre-purchase inspection. While many used cars are in good condition, some may have underlying issues that could affect their performance or safety. To mitigate this risk, it’s crucial to have a trusted mechanic inspect the car before you purchase it.

Conclusion

Ultimately, the decision to finance a new or used car depends on your budget, preferences, and long-term goals. If you value reliability, advanced features, and a warranty, a new car may be the right choice for you. On the other hand, if you’re looking for lower payments, slower depreciation, and reduced insurance costs, financing a used car could be the better option.

Regardless of your decision, it’s important to do thorough research, understand the total cost of ownership, and make sure that the financing terms work within your budget. By weighing the pros and cons of both new and used car financing, you can make an informed choice that aligns with your financial situation and personal needs.