Traveling can be an exciting and enriching experience, but it also presents certain risks, especially when it comes to health. Accidents, illnesses, or medical emergencies can occur when you least expect them, and if you’re traveling abroad, the situation can become more complicated. That’s why having the right health insurance coverage while traveling is essential. Whether you’re going on a weekend getaway or embarking on an extended overseas adventure, understanding how health insurance works for travelers is crucial. This article will guide you through the various types of health insurance for travelers, the importance of coverage, and how to make the best choice for your trip.

The Importance of Health Insurance for Travelers

Health insurance for travelers is vital because many domestic health insurance plans do not offer full coverage outside of the country or even outside your home state. Healthcare systems and costs differ greatly from one country to another, and the medical care you may receive abroad might not meet the same standards you’re accustomed to. More importantly, many foreign healthcare providers may require payment upfront before offering medical services, and your regular health insurance might not reimburse you for these expenses.

Without health insurance while traveling, you could face significant out-of-pocket expenses, or worse, be unable to get medical treatment in a timely manner. For these reasons, having the right coverage provides peace of mind, ensuring that if something goes wrong, you’ll be protected financially and medically.

Types of Travel Health Insurance

Travel health insurance comes in several forms, depending on your needs, the length of your trip, and your destination. Below are the most common types of travel health insurance:

- Single-Trip Travel Insurance: This type of health insurance is designed for a one-time trip. You’ll purchase coverage for the specific dates you’ll be traveling, and the policy will provide medical care benefits during that period. This is ideal for travelers who only take occasional vacations or business trips. It covers a variety of incidents like emergency medical treatment, hospital stays, emergency evacuation, and repatriation if you need to return home for health reasons.

- Multi-Trip/Annual Travel Insurance: If you travel frequently throughout the year, multi-trip or annual travel insurance can offer a more cost-effective solution. Instead of purchasing separate insurance for each trip, an annual plan covers multiple trips over a set period (typically one year). It provides the same benefits as single-trip insurance, but you won’t have to worry about buying a new policy for each trip. This is an excellent choice for those who travel for business or leisure several times a year.

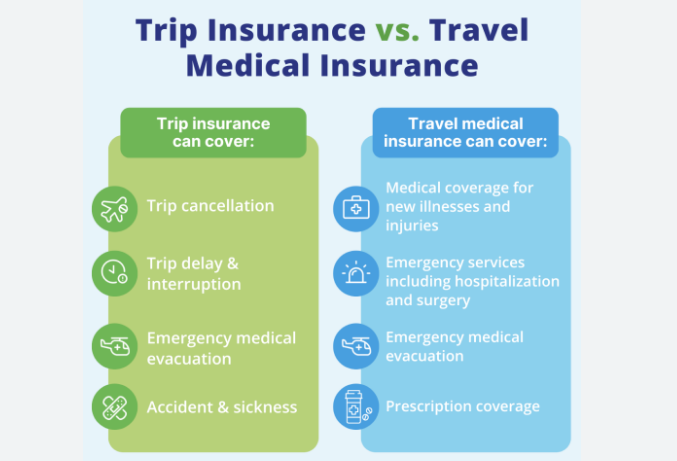

- Travel Medical Insurance: This is a specialized insurance that only covers medical expenses incurred while traveling. It is ideal for individuals who are looking for basic health coverage during their trips, but it does not typically cover other travel-related issues like trip cancellations, lost luggage, or flight delays. Travel medical insurance may include emergency medical treatment, hospital stays, and emergency medical evacuation if necessary.

- Comprehensive Travel Insurance: Comprehensive travel insurance packages offer a broader range of coverage. In addition to medical coverage, these policies often include trip cancellation and interruption, lost baggage, flight delays, emergency evacuation, and other non-medical travel-related incidents. While comprehensive insurance is typically more expensive than travel medical insurance alone, it offers greater peace of mind, especially for travelers concerned about a wide range of potential issues during their trip.

- Long-Term Travel Insurance: If you’re planning an extended overseas trip, such as backpacking for several months or taking a gap year, long-term travel insurance is designed to provide coverage for extended durations. Long-term travel insurance offers both medical and non-medical coverage for a prolonged period, often up to a year or more. It can be customized based on your specific needs, including trip duration, activities you plan to do, and your destination.

What Does Travel Health Insurance Typically Cover?

Travel health insurance policies vary in their coverage, but most offer similar core benefits. Some of the most common areas of coverage include:

- Emergency Medical Treatment: If you fall ill or suffer an injury while traveling, travel health insurance will cover the cost of emergency medical treatment. This includes hospital visits, surgeries, medications, and any other necessary medical interventions during your trip. If your health insurance plan doesn’t cover international treatment, this is crucial coverage.

- Emergency Medical Evacuation: In certain situations, such as serious illness or injury, you may need to be transported to a medical facility in a nearby city or country with better treatment options. Emergency medical evacuation ensures that you receive the necessary transportation, whether by ambulance, airlift, or another means of transport.

- Repatriation of Remains: If a traveler passes away while abroad, the cost of returning their remains to their home country can be incredibly expensive. Travel health insurance policies often provide coverage for the repatriation of remains, relieving the financial burden from the family.

- Trip Cancellation and Interruption: While not specifically a medical benefit, many comprehensive travel insurance plans include trip cancellation or interruption coverage. If you need to cancel or cut short your trip due to a medical emergency or other valid reasons, this coverage reimburses you for non-refundable costs, such as flights, hotels, and tours.

- Prescription Medications: If you require prescription medications while traveling, most policies will help cover the cost of necessary prescriptions, including refills if you run out while abroad.

- Dental Emergencies: Some travel insurance policies also include coverage for dental emergencies, which can be particularly important if you experience sudden dental pain or injury while abroad.

What Does Travel Health Insurance Not Cover?

While travel health insurance can provide a wide range of benefits, it does not cover everything. Some common exclusions from travel insurance policies include:

- Pre-existing Medical Conditions: Most travel insurance policies do not cover illnesses or injuries that are related to pre-existing medical conditions. However, some providers offer policies that include limited coverage for pre-existing conditions, often for an additional premium. It’s important to review the terms of your policy and disclose any pre-existing conditions before purchasing.

- Routine and Non-Emergency Care: Travel insurance typically does not cover routine medical care such as annual check-ups, vaccinations, or non-emergency procedures. If you need ongoing care for a chronic condition while abroad, you’ll likely need to seek out local healthcare options.

- Adventure Sports or High-Risk Activities: If you’re planning to engage in high-risk activities such as skydiving, scuba diving, or mountain climbing, you may need to purchase a policy that specifically covers these activities. Regular travel health insurance often excludes injuries resulting from extreme sports.

- Alcohol or Drug-Related Incidents: Many policies exclude coverage for medical issues caused by alcohol or drug consumption. If your injury or illness is linked to substance abuse, your claim may be denied.

How to Choose the Right Travel Health Insurance

Choosing the right travel health insurance policy depends on several factors, including the destination, the duration of your trip, your health condition, and the activities you plan to do. Consider the following when selecting a policy:

- Destination: Healthcare standards and costs vary from country to country. If you’re traveling to a region with high healthcare costs or limited access to medical facilities, you may need a more comprehensive policy.

- Trip Length: For short trips, a single-trip policy may suffice. However, if you’re traveling for several months or longer, long-term or multi-trip insurance may offer better value.

- Medical History: If you have pre-existing conditions, make sure the policy covers them or look for options that provide specific coverage for such conditions.

- Activity Level: If you plan to engage in high-risk activities, ensure your insurance provider offers coverage for these activities.

- Policy Limits and Exclusions: Carefully read the terms and conditions of the policy, particularly the exclusions and limits on coverage. Look for policies that offer adequate coverage for your needs and avoid ones with overly restrictive terms.

Conclusion

Health insurance for travelers is a critical consideration that ensures your safety and financial protection while on the move. By choosing the right travel health insurance policy, you can travel with confidence, knowing that you’re covered in case of medical emergencies, accidents, or unexpected health issues. Whether you’re planning a short vacation or a long-term adventure, having the appropriate health insurance provides peace of mind, allowing you to focus on enjoying your trip instead of worrying about what might go wrong. Always research your options thoroughly and select a policy that suits your needs and travel plans to ensure a safe and enjoyable journey.